Piecing It Together, May 21

For the most recent commentary from our friends and colleagues at One Capital Management

click on the link below.

http://www.onecapital.com/webcast_08.html

to discuss this or any other Wealth Management Issues

jstomenson@wellwest.ca

http://www.jstomenson.com/

Tuesday, May 25, 2010

Wednesday, May 12, 2010

An Investor’s Odyssey Is Never a Smooth Ride

An Investor’s Odyssey Is Never a Smooth Ride

May 10, 2010

Last week saw volatility return to equity markets after a long hiatus. The VIX Index, which measures the implied volatility of equities based on options on the S&P500 index, spiked to a level of 42.15 on May 7. While the level was nowhere near as high as that reached following the bankruptcy of Lehman Brothers in September 2008, it serves to remind investors that the global financial crisis that started a year and half ago is not entirely behind us.

In this instance, the small Mediterranean nation of Greece instigated the market sell-off. After months of negotiations between Greece and its fellow European Union members, the country agreed last week to adopt punishing austerity measures in exchange for a $US 143 billion bailout package backed by the EU and International Monetary Fund. While Greece’s fiscal woes have been understood for some time, markets were jolted by the final size of the bailout, the resulting public protests and the potential implications for EU members in similar fiscal situations, namely Portugal, Italy, and Spain. As was the case with Lehman, markets are concerned that Greece is the canary in the coal mine warning greater market declines.

Opposing these sovereign debt issues is continued improvement in economic and equity fundamentals. Statistics Canada reported that 108,700 new jobs were added in Canada in April, bringing the employment rate down by 0.1%. In the U.S., while the unemployment rate inched higher, data pointed to improvement in consumer spending with a 0.6% increase in March – the most in five months. Manufacturing also saw continued expansion with the Institute for Supply Management’s index rising to 60.4, indicating the ninth straight month of expansion. At nearly the end of earnings season, we also received news that 77% of S&P500 companies have reported earnings better than analysts’ estimates. And at the time of writing, the EU unveiled a $960 billion rescue fund for to backstop EU governments in financial distress.

In April, we wrote that this was a time of contradiction – with good and bad news fighting for investors’ attention. The events in Europe, while unsettling, do not shake us from our conviction that investors are best served by holding high quality stocks and not attempting to time the market. The pain of market timing can most certainly be felt by those that sold into the weekend only to see markets rebound on Monday. Rather, at Wellington West Asset Management Inc., we have structured our Canadian and US equity portfolios to benefit from improving equity markets, but with reduced downside risk should the bull market of 2009/10 take a pause.

Sources: Bloomberg, Wall Street Journal, Financial Times

Wellington West Asset Management Inc.

www.wellingtonwest.com

Graeme Hay, CMA

Investment AnalystWellington West Asset Management Inc.

www.jstomenson.ca

May 10, 2010

Last week saw volatility return to equity markets after a long hiatus. The VIX Index, which measures the implied volatility of equities based on options on the S&P500 index, spiked to a level of 42.15 on May 7. While the level was nowhere near as high as that reached following the bankruptcy of Lehman Brothers in September 2008, it serves to remind investors that the global financial crisis that started a year and half ago is not entirely behind us.

In this instance, the small Mediterranean nation of Greece instigated the market sell-off. After months of negotiations between Greece and its fellow European Union members, the country agreed last week to adopt punishing austerity measures in exchange for a $US 143 billion bailout package backed by the EU and International Monetary Fund. While Greece’s fiscal woes have been understood for some time, markets were jolted by the final size of the bailout, the resulting public protests and the potential implications for EU members in similar fiscal situations, namely Portugal, Italy, and Spain. As was the case with Lehman, markets are concerned that Greece is the canary in the coal mine warning greater market declines.

Opposing these sovereign debt issues is continued improvement in economic and equity fundamentals. Statistics Canada reported that 108,700 new jobs were added in Canada in April, bringing the employment rate down by 0.1%. In the U.S., while the unemployment rate inched higher, data pointed to improvement in consumer spending with a 0.6% increase in March – the most in five months. Manufacturing also saw continued expansion with the Institute for Supply Management’s index rising to 60.4, indicating the ninth straight month of expansion. At nearly the end of earnings season, we also received news that 77% of S&P500 companies have reported earnings better than analysts’ estimates. And at the time of writing, the EU unveiled a $960 billion rescue fund for to backstop EU governments in financial distress.

In April, we wrote that this was a time of contradiction – with good and bad news fighting for investors’ attention. The events in Europe, while unsettling, do not shake us from our conviction that investors are best served by holding high quality stocks and not attempting to time the market. The pain of market timing can most certainly be felt by those that sold into the weekend only to see markets rebound on Monday. Rather, at Wellington West Asset Management Inc., we have structured our Canadian and US equity portfolios to benefit from improving equity markets, but with reduced downside risk should the bull market of 2009/10 take a pause.

Sources: Bloomberg, Wall Street Journal, Financial Times

Wellington West Asset Management Inc.

www.wellingtonwest.com

Graeme Hay, CMA

Investment AnalystWellington West Asset Management Inc.

www.jstomenson.ca

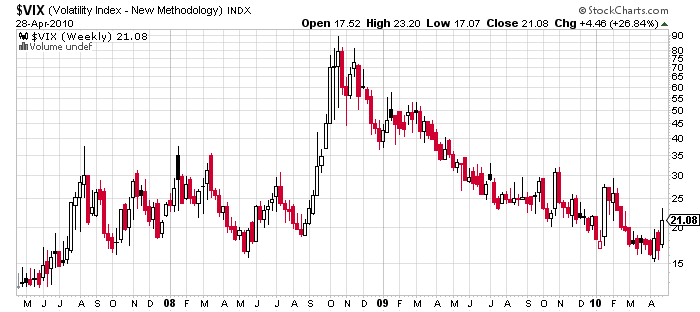

Thursday, April 29, 2010

Is your portfolio ready for an increase in volatility?

Is your portfolio ready for an increase in volatility?

When the market hit maximum uncertainty in late 2008, volatility spiked to extreme levels. Since then volatility has declined substantially.

When the market hit maximum uncertainty in late 2008, volatility spiked to extreme levels. Since then volatility has declined substantially.

While there has been some sustained gradual global economic recovery, lead by emerging markets (and this is expected to continue), there are growing uncertainties being caused by Europe’s sovereign debt crisis that could play havoc with investors confidence, thus turning the trend in volatility.

In my experience, an increase in volatility tends to lead to a change in trend. We are almost 14 months into the up-trend that started in early March 2009.

If I have learned anything in my 28 years as an investment professional, it is that complacency is everyone’s enemy. We must always be on guard for the unexpected. While there is never absolute certainty that a trend will change, we must always be on guard for it. Most times, like in late 2008, you won’t know what hit you until it has already run you over!

So I preach diversity and balance as a portfolio protector from volatility.

Diversity across asset classes: bonds and preferred shares for yield, equities for growth. When equities don’t provide growth, bond income and preferred dividends will.

Diversity across global economies: emerging economies are leading the recovery, but US equities have been leading the stock market.

Diversity across company size: US small and micro cap companies are leading the US equity markets.

When you get “outperformance” by one asset class, then you rebalance to redistribute portfolio profitability to the underperforming sectors that will not remain underperforming forever.

Volatility will return, I can’t say exactly when, but when it does, be prepared!

I can help:

www.jstomenson.com

Monday, April 12, 2010

Envision your Future 2 , Thurs. April 15, 1pm.

Webcast envision Your Future, Thursday April 15th, 1pm.

“a glimpse into your future, a planning tool, more certainty, comfort and peace of mind."

1. Please join my meeting.https://www1.gotomeeting.com/join/586104608

2. Join the conference call:

Local Dial-in number: 416-343-2285

Toll-free Dial-in number: 1 877-969-8433

Conference ID: 9764038

“a glimpse into your future, a planning tool, more certainty, comfort and peace of mind."

1. Please join my meeting.https://www1.gotomeeting.com/join/586104608

2. Join the conference call:

Local Dial-in number: 416-343-2285

Toll-free Dial-in number: 1 877-969-8433

Conference ID: 9764038

Thursday, March 11, 2010

Envision Your Future

Webinar:

http://www.wellwest.ca/ww_dl/Meet_Now.wmv

“a glimpse into your future, a planning tool, more certainty, comfort and peace of mind."

www.jstomenson.ca

http://www.wellwest.ca/ww_dl/Meet_Now.wmv

“a glimpse into your future, a planning tool, more certainty, comfort and peace of mind."

www.jstomenson.ca

Wednesday, February 24, 2010

What Frustrates you most about banking?

What frustrates you most about banking?

If you have a mortgage and a chequing or savings account (with the same institution), what is the spread they are they are taking on you?

What is your mortgage cost (interest rate): 4% perhaps?

What are they paying you for the money that you are lending them back in your chequing account? 0% (they get this money from you for free).

In your savings account? 0 .5%.

So the spread they are taking on you in this scenario is 3.5% to 4%.

If you have a mortgage of $250,000 and savings of 40,000 (savings account), your net borrowing should be $210,000 if you were able to apply your savings to your mortgage. You would be paying approximately $1400 less per year in interest costs (that are not tax deductible). That adds up over time.

So why do the banks not let you do this?

They don’t want to lose the free $1400.

Then there are the fees and don’t forget the gouging spread on foreign exchange.

I can help solve the first issue and generate very good ideas for flexibility in your cash flow, especially if you have a variable income stream.

Of course: cash flow is the engine that drives a financial plan.

If you want to explore any of these options, let me know, we build Wealth Forecasts to show you how to maximize efficiencies in your financial plan and mitigate risk in your investment portfolio.

jstomenson@wellwest.ca

www.jstomenson.ca

http://www.financialpost.com/magazine/story.html?id=2514256

If you have a mortgage and a chequing or savings account (with the same institution), what is the spread they are they are taking on you?

What is your mortgage cost (interest rate): 4% perhaps?

What are they paying you for the money that you are lending them back in your chequing account? 0% (they get this money from you for free).

In your savings account? 0 .5%.

So the spread they are taking on you in this scenario is 3.5% to 4%.

If you have a mortgage of $250,000 and savings of 40,000 (savings account), your net borrowing should be $210,000 if you were able to apply your savings to your mortgage. You would be paying approximately $1400 less per year in interest costs (that are not tax deductible). That adds up over time.

So why do the banks not let you do this?

They don’t want to lose the free $1400.

Then there are the fees and don’t forget the gouging spread on foreign exchange.

I can help solve the first issue and generate very good ideas for flexibility in your cash flow, especially if you have a variable income stream.

Of course: cash flow is the engine that drives a financial plan.

If you want to explore any of these options, let me know, we build Wealth Forecasts to show you how to maximize efficiencies in your financial plan and mitigate risk in your investment portfolio.

jstomenson@wellwest.ca

www.jstomenson.ca

http://www.financialpost.com/magazine/story.html?id=2514256

Monday, February 1, 2010

Do more of that which is working

“Do more of that which is working and less of that which is not”!

That is one of Dennis Gartman’s 20 rules of trading. Dennis Gartman, if you do not already know, is a widely read and admired market commentator who writes a daily letter to which I subscribe and it is the first reading on my agenda every morning. Ever insightful and informational on a variety of topics: markets, currencies, commodities, economics and politics.

Every year on the Friday after US Thanksgiving he publishes his 20 rules of trading.

“Do more of that which is working and less of that which is not”!

So what is working?

1) Clients both old and new are slowly coming around to the idea of seeing their “Wealth Forecast”.

a. Generally speaking, this is a spreadsheet that we create that shows clients their income streams now and those that are forecasted for their future vs. their desired or expected lifestyle needs (cost of living) and then analyzes what the approximate impact will be on their assets.

b. We make a number of adjustable assumptions on things like return (after fees and taxes), inflation, tax rates and we create a “working model” from which we can project 10, 20, 30 or more years into the future.

c. We have the ability to create a number of different models that represent scenarios from which we can select the most advantageous options.

d. From this we have a full understanding of the clients risk profile.

e. We make the appropriate asset allocation strategy and implement it.

f. What we have is our “benchmark” from which we can gage the client’s progress.

g. If (as we fully expect there will be) there are any changes that need to be addressed we can quickly re-asses strategy by making adjustments and visualizing their impact on our model, followed-up with an adjustment of strategy.

2) While we believe that over the longer term, 5 to 10 years, equity markets will resume their upward trajectory, we also know that:

a. Clients have cash needs (from their assets)

b. Depending on specific needs, we believe that a diversified, balanced portfolio will allow easier access to client assets for these purposes.

c. Where are we finding balance and low volatility (i.e.while equity markets are down, what is up) ?

i. One Capital Management, managed portfolios

ii. Waterfront Nxt Income and Growth

iii. Norrep Yield Fund

Visit our website at www.jstomenson.ca

Envision your future

That is one of Dennis Gartman’s 20 rules of trading. Dennis Gartman, if you do not already know, is a widely read and admired market commentator who writes a daily letter to which I subscribe and it is the first reading on my agenda every morning. Ever insightful and informational on a variety of topics: markets, currencies, commodities, economics and politics.

Every year on the Friday after US Thanksgiving he publishes his 20 rules of trading.

“Do more of that which is working and less of that which is not”!

So what is working?

1) Clients both old and new are slowly coming around to the idea of seeing their “Wealth Forecast”.

a. Generally speaking, this is a spreadsheet that we create that shows clients their income streams now and those that are forecasted for their future vs. their desired or expected lifestyle needs (cost of living) and then analyzes what the approximate impact will be on their assets.

b. We make a number of adjustable assumptions on things like return (after fees and taxes), inflation, tax rates and we create a “working model” from which we can project 10, 20, 30 or more years into the future.

c. We have the ability to create a number of different models that represent scenarios from which we can select the most advantageous options.

d. From this we have a full understanding of the clients risk profile.

e. We make the appropriate asset allocation strategy and implement it.

f. What we have is our “benchmark” from which we can gage the client’s progress.

g. If (as we fully expect there will be) there are any changes that need to be addressed we can quickly re-asses strategy by making adjustments and visualizing their impact on our model, followed-up with an adjustment of strategy.

2) While we believe that over the longer term, 5 to 10 years, equity markets will resume their upward trajectory, we also know that:

a. Clients have cash needs (from their assets)

b. Depending on specific needs, we believe that a diversified, balanced portfolio will allow easier access to client assets for these purposes.

c. Where are we finding balance and low volatility (i.e.while equity markets are down, what is up) ?

i. One Capital Management, managed portfolios

ii. Waterfront Nxt Income and Growth

iii. Norrep Yield Fund

Visit our website at www.jstomenson.ca

Envision your future

Subscribe to:

Posts (Atom)

{kind=link}