Blockbuster Day Of Economic News Yesterday

First of the day, was U.S. GDP, which slowed to an annualized growth rate of 2% and would have perhaps been somewhat lower if consumers were not busy buying recreational goods and vehicles (at a 17% clip).

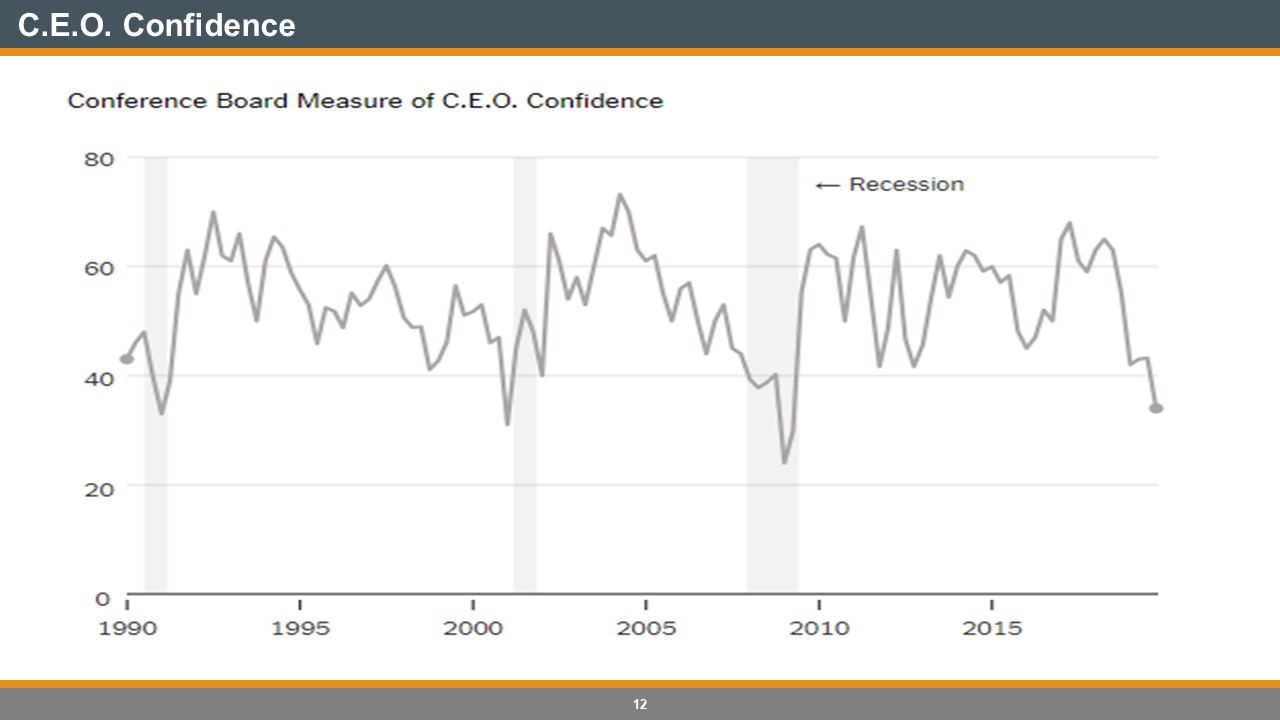

Interesting, when just the day before, the Conference Board's index of consumer confidence (forward looking) hit a four month low. Is that it for the U.S. consumer?

As expected, the U.S. Federal Reserve dropped the Fed funds rate by 1/4%. However they also suggested that they are done for now. Although, that will of course be dependent on future economic data, but the easing of trade and Brexit concerns (at least on the surface) has given Fed Chair Powell some breathing room, perhaps. This morning though, Chinese officials are apparently suggesting that they don't see a long-term deal happening with President Trump at the helm. So the saga continues. I can't say that making crucial investment decisions has been made any easier.

The Bank of Canada left rates unchanged. However, thy were decidedly down-beat about their outlook: "In today's updated projections, we are forecasting both exports and business investment to contract in the second half of this year and to recover only moderately in the next two years."

This morning the August Canadian GDP data came in at a lower than expected 0.1% rate of growth and while we have to wait for September's data (not sure why it takes Stats Can so long to get to it) until we see full Q3 results (in another month!), it would appear that somewhere around a 1.3% annual growth rate is in the cards. Hardly impressive (especially with inflation outpacing economic growth).

So why is the BOC sitting on its hands? My guess is that Canadians have just too much debt and they are reluctant to encourage them to take on any more: "the recent strength in many housing markets across the country is a reminder that we will be carrying high levels of debt for a long time, despite a constructive evolution of vulnerabilities".

In the end, they are "mindful that the resilience of Canada's economy will be increasingly tested as trade conflicts and uncertainty persist".

Well that does not help us much in making those crucial investment decisions, does it?

With 2% and falling growth in the U.S. , 1.3% and falling growth in Canada, 1.1% and falling growth in the Eurozone and China's economy growing at about 17 year lows (and Hong Kong is in recession), there is not a great deal of opportunity (at the moment) to get the balanced portfolio close to it's multi-year averages: up to it's 6-7% annual average growth rate, without taking on mountains of additional risk (stock markets at their highs = big risk in the short-term).

That time will definitely come (long-term investors will benefit), but in the interim, protecting your capital should be your first priority.